2024 is off to an exciting start and we wanted to share our quarterly Markets in Motion that incorporates all of our SMA product offerings (fundamental, rules-based, & blended strategies). This brings our entire investment ecosystem under one commentary and provides easier access to information for our clients. We will continue to publish monthly Markets in Motion pieces to discuss market conditions as they evolve and will provide trade updates for all strategies. We are committed to providing risk managed and transparent solutions to all our clients.

The Macro is Changing

At the start of 2024, the US seemed to be settling into a disinflationary boom. Economic growth and earnings growth were both robust and inflation had slowed dramatically.

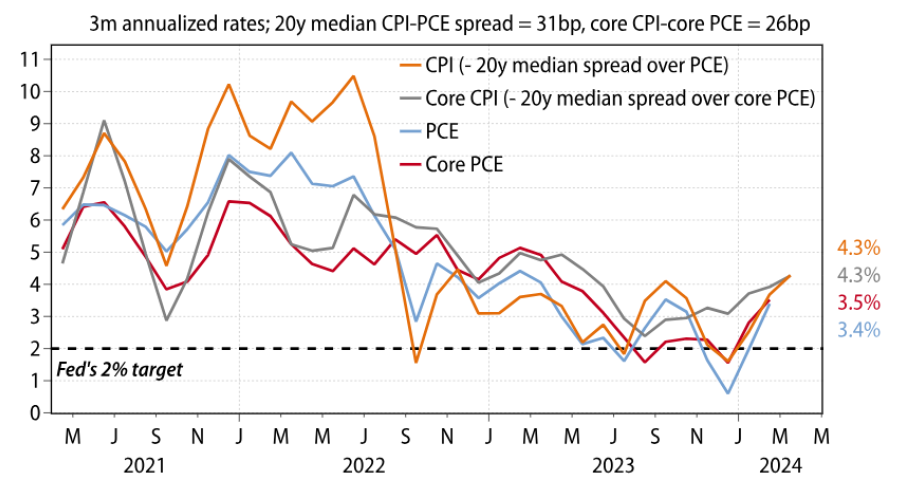

Growth and earnings have held up (so far), but inflations trend is changing. In the last three months of 2023, annualized inflation rates for CPI, PCE and core PCE all averaged below the Fed’s 2% target. This pushed the Fed to pivot policy and raised expectations for rate cuts as soon as March 2024.

However, over the first three months of 2024, headline CPI rose at an annualized rate of 4.6%, while core CPI rose 4.5%. Both are now at their highest since June 2023. This qualifies as enough of a trend to significantly delay rate cuts, if not take them off the table entirely. In short, the macro backdrop is no longer supportive of easier policy. If US inflation data remains sticky, it could spook policymakers and markets. (Chart 1)

US Inflation rates have reaccelerated

(Chart 1) Source: Gavekal Research/Macrobond

We have already seen financial conditions tighten as a result of the hotter than expected reports. The 10-yr treasury yield, the price of oil, and the US dollar are three of the most important financial conditions we monitor. All three had been heading lower for the better part of Q4 2023, but recently they have all been ticking higher again, and the stock market is acting heavier and heavier the higher they go. (Chart 2)

(Chart 2) Source: Bespoke

If the combination of strong growth, reaccelerating inflation, and a more hawkish fed continue to push bond yields, USD, and oil higher, this could eventually weigh on growth stocks which by definition are long-duration assets. This group of stocks have buoyed the large rally since the end of 2022, and weakness in leadership will weigh on indices.

A potentially larger concern is the reheating of the economy actually increasing the odds that the economy will fall into a recession. We have discussed this balancing act in past commentary, but more hawkish policy could force the Fed to throw too much cold water on the economy (at the exact wrong time), eventually leading it to freeze over. Contrary to popular perception, we believe the odds of a global recession over the next 12 months are rising, not falling.

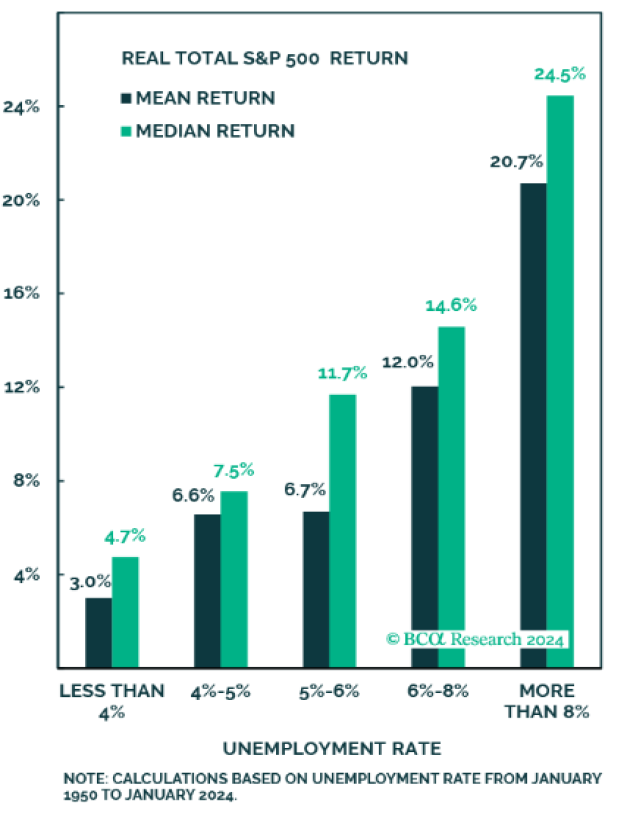

Starting points matter, and with valuations stretched, taking too much equity risk could be costly. In fact, one might think stocks fare best when unemployment is low. But the S&P500 has consistently produced better returns when the unemployment rate is high rather than low. (Chart 3)

Average Annualized 1-Month Real Total S&P 500 Return

(Chart 3) Source: BCA

One reason is that equity valuations tend to become stretched when times are great, and unemployment is low. A more ominous reason is that the unemployment rate is a highly mean-reverting series. When it gets down to very low levels, it usually starts rising again. In short, recessions always start from low unemployment and bear markets always start from all-time highs.

Long-Term: A New Investing Paradigm

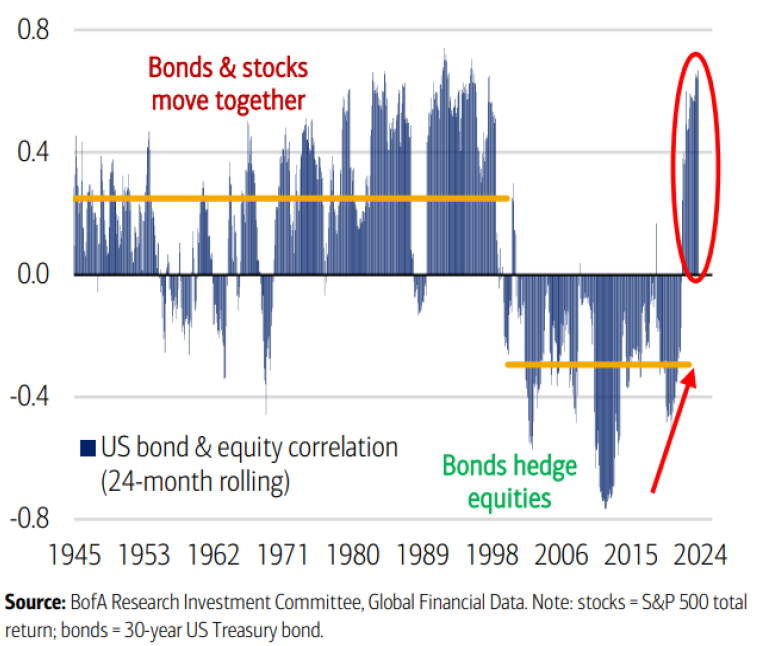

We have mentioned this in past commentary, but we believe it’s worth repeating. Bond and stock correlation has been near 1:1 for almost 3 years now. And historically, this has generally been the case other than the great disinflation of the past two decades. (Chart 4).

Rolling 24-month correlation between US stocks and Treasury bonds

(Chart 4) Source: BofA Research Investment Committee, Global Financial Data. Note: stocks = S&P 500 total return; bonds = 30 year US treasury bond

If it is indeed a new normal, then the long-term implications for portfolio management are dramatic. After all, most pension funds, insurance companies and private portfolios are built on the premise that exposure to bonds reduces portfolio volatility and limits downside risks. While short-term we could see treasuries act as a safe haven during the next recessionary cycle, longer term investors will need to adapt portfolios to achieve diversification and client goals. “Buy and Hold forever” is no longer a reasonable strategy for many fixed income asset classes.

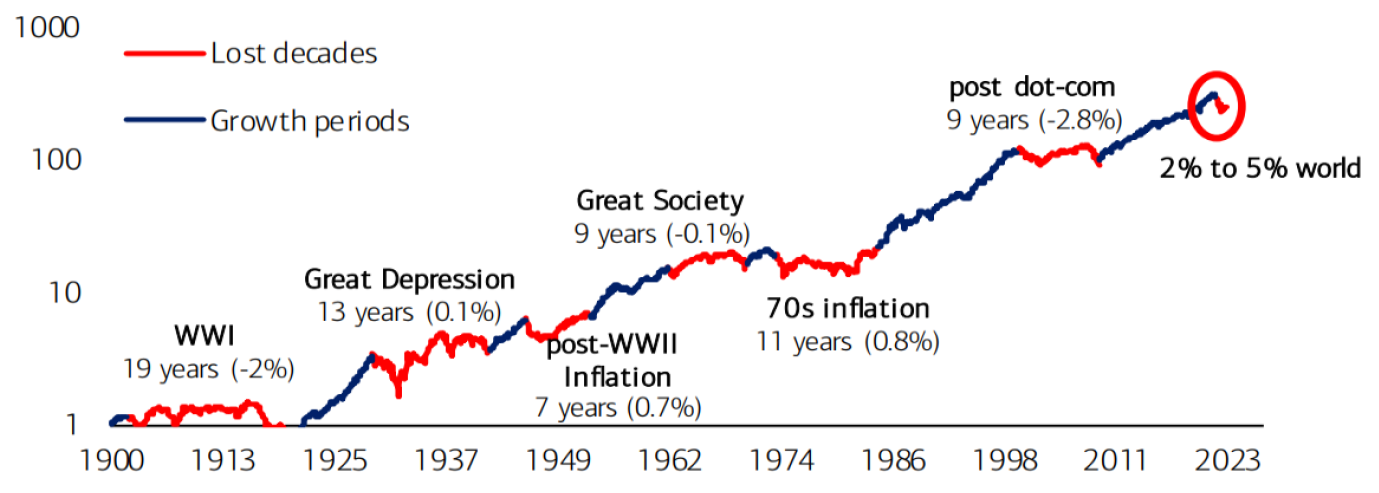

We believe the importance of tactical asset allocation will be critical to clients meeting their long-term objectives. A 60% equity and 40% bond portfolio, the guidepost of moderate strategic asset allocation, has experienced multiple “lost decades” over history. (Chart 5).

Cumulative performance of a 60/40 portfolio, real prices, log scale

(Chart 5) Source: BofA Research Investment Committee, Global Financial Data. Note: 60/40 = 60% S&P 500 total return and 40% US 10-year bond total return.

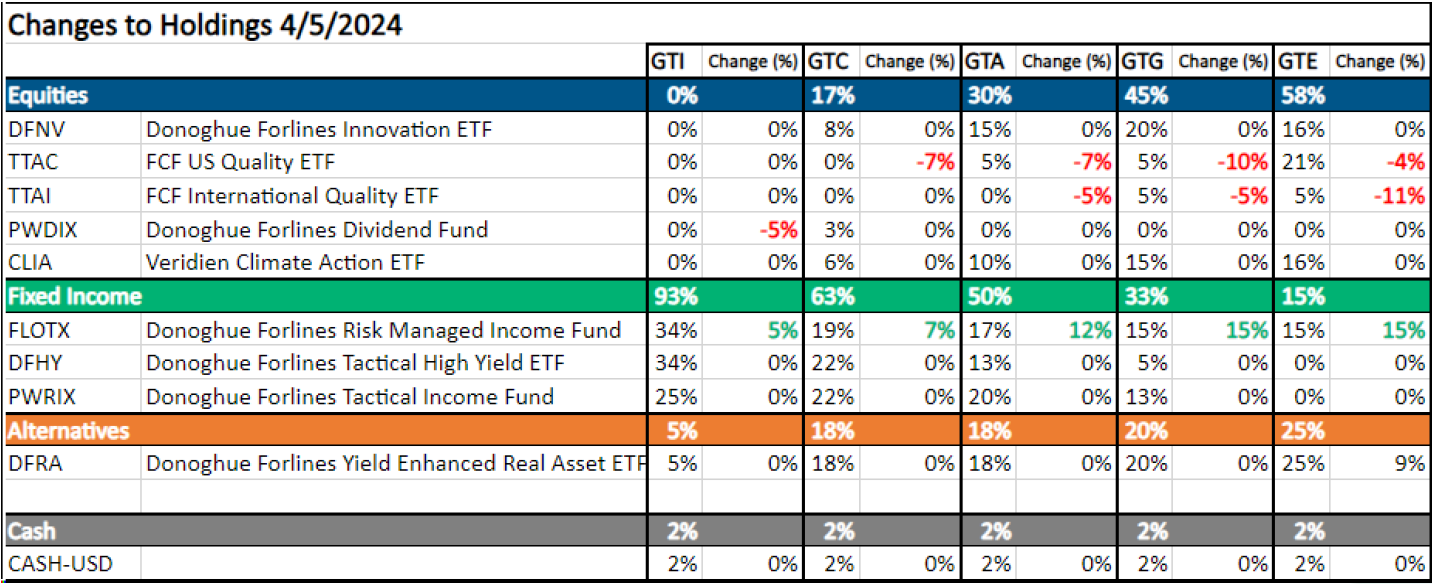

(Positioning as of 4/5/2024)

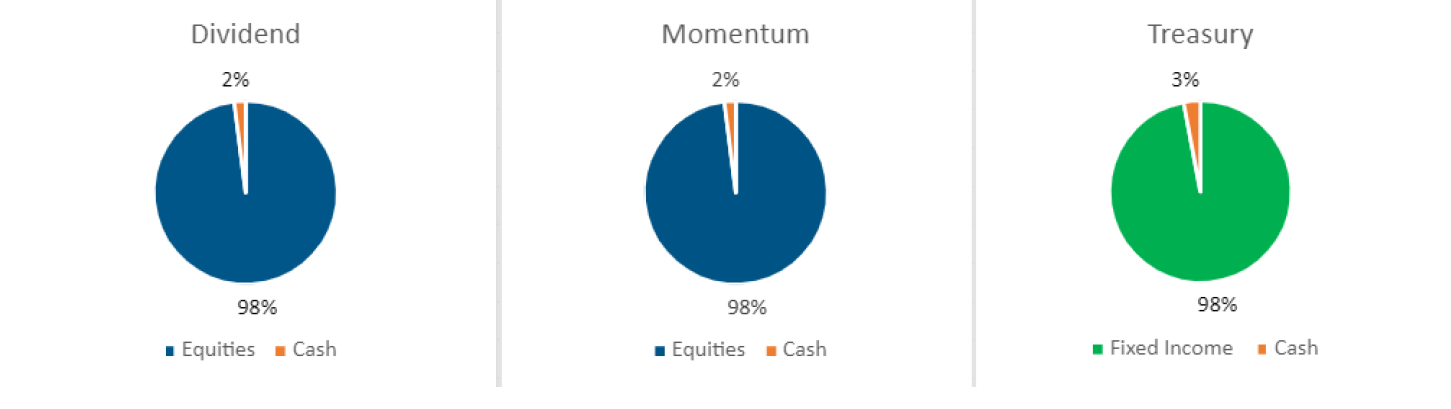

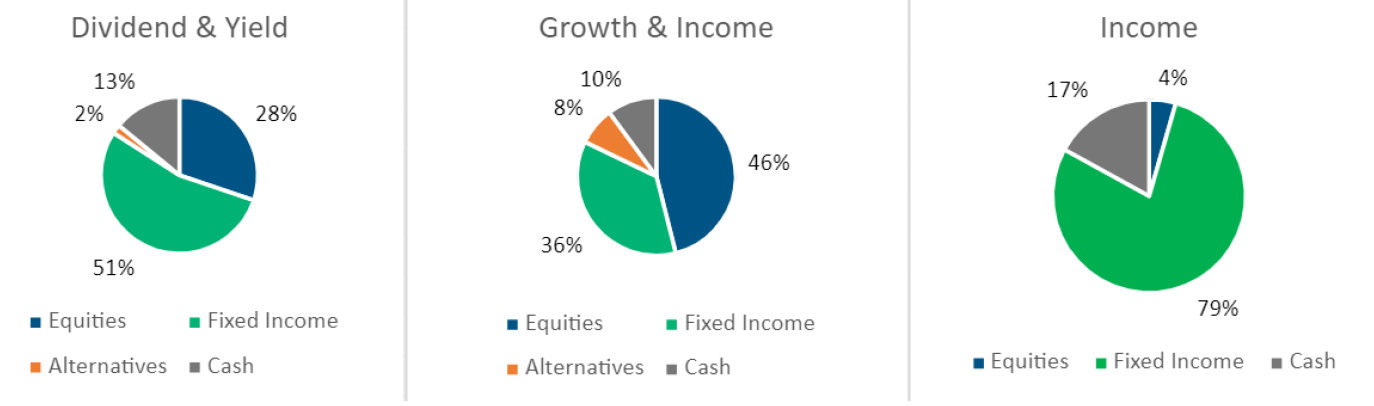

Rules Based Portfolios

The technical picture for equities remains strong with long-term trends remaining intact.

Our Momentum strategy remained fully invested in equities throughout the quarter and was able to take advantage of the risk-on environment. The strategy’s performance ranked in the top 1% in its category YTD, and in the top 2% of its category for 1-year trailing performance. The technical picture for growth stocks remains in an uptrend and would likely need to see quick price deterioration to trigger a more defensive posture.

Our Dividend strategy remained fully invested in equities throughout the quarter and was able to take advantage of the risk-on environment. The technical picture for value equities remains in an uptrend but is weaker than stocks broadly. If markets were to turn, we could see the Dividend strategy move to a defensive posture more quickly. We believe dividend stocks are poised to outperform broader equities for the remainder of 2024.

Our Treasury strategy remained in shorter duration instruments for the entirety of the quarter. Rates have broken out again and we avoided the sell-off in longer duration bonds. We expect to allocate to longer duration bonds more frequently for the remainder of 2024.

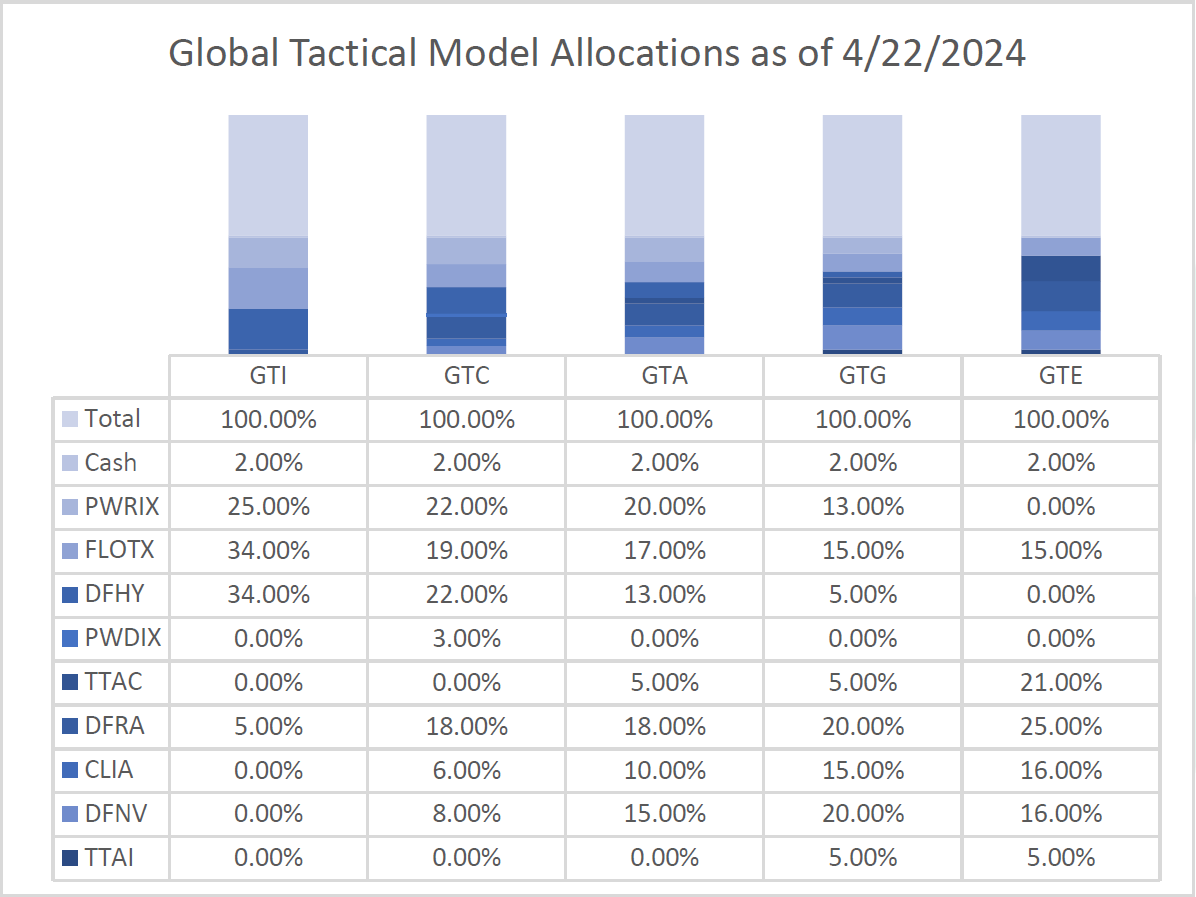

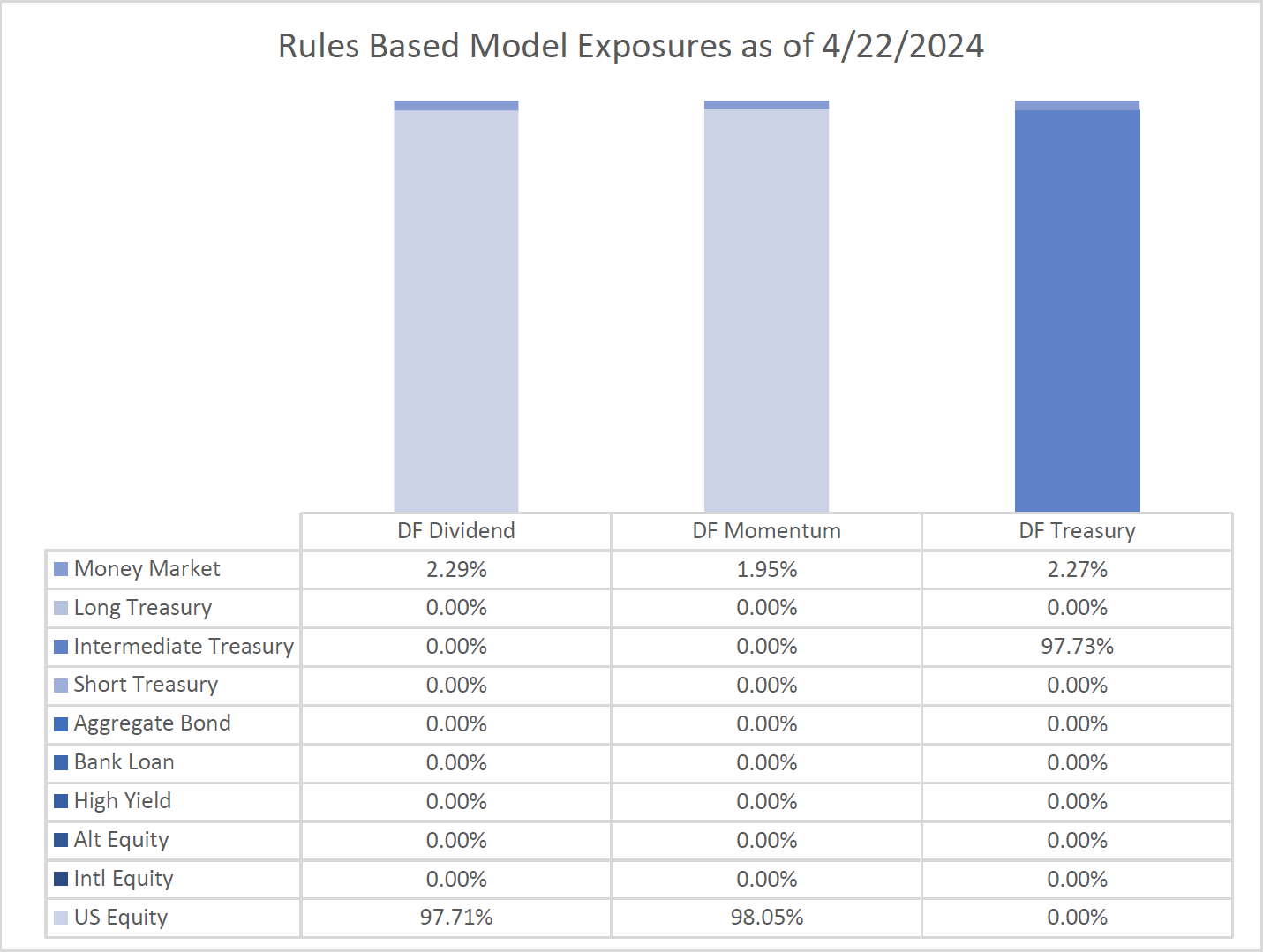

(Positioning as of 4/22/2024)

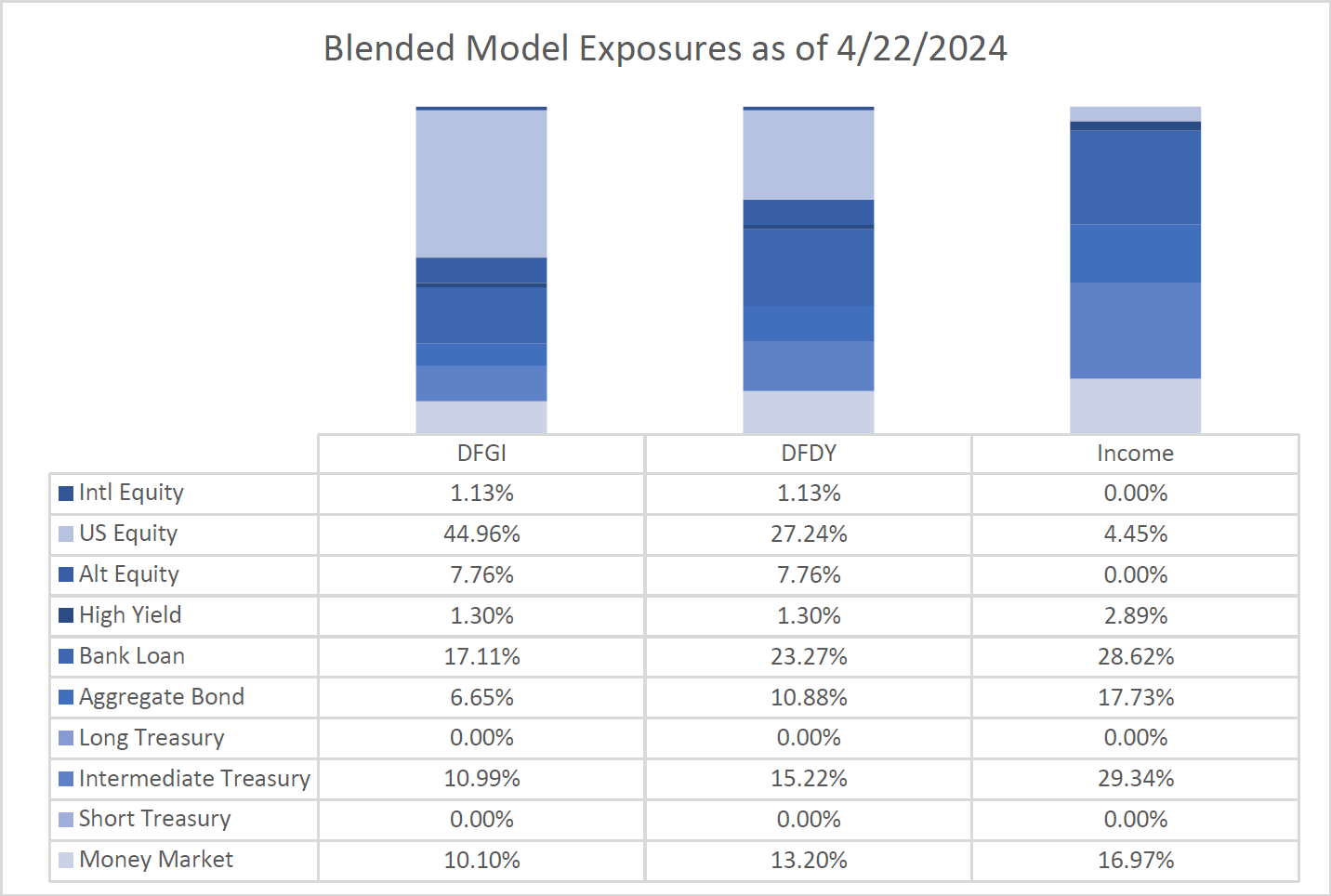

Blended Portfolios

The blended portfolios are a proprietary mix of our fundamental macro portfolios and our rules-based quantitative portfolios.

Through this combination, we were able to take advantage of the sanguine risk environment in the first quarter of 2024. Our top-down asset allocation mirrored our fundamental outlook and overweighted our tactical allocation and tactical income funds in the strategies, where we were neutral to risk in equities & credit. Our momentum fund was a powerful driver of performance.

Heading into the rest of 2024 our top-down asset allocation mirrors our fundamental outlook – positioned underweight to risk. Our equity rules-based strategies are currently fully invested, and our risk managed income fund is positioned in cash equivalents and floating rate securities. We recently decreased allocations to our equity funds, selling out of our momentum fund, and increased allocations to tactical fixed income funds.

We will adapt as the facts change and focus on catalysts for investment regime change.

(Positioning as of 4/22/2024)

You can get more information by calling (800) 642-4276 or by emailing AdvisorRelations@donoghueforlines.com.

Best regards,

Best regards,

John A. Forlines III

Chief Investment Officer

IMPORTANT RISK INFORMATION

Past performance is no guarantee of future results. Performance prior to January 1, 2018 was earned on accounts managed at a predecessor firm, JAForlines Global. The person primarily responsible for achieving that performance continues to manage accounts at Donoghue Forlines in a substantially similar manner. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. The investment descriptions and other information contained in this Markets in Motion are based on data calculated by Donoghue Forlines LLC and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate. The calculation and presentation of performance has not been approved or reviewed by the SEC or its staff.

The Donoghue Forlines Global Tactical Allocation Portfolio composite was created July 1, 2009. The Donoghue Forlines Global Tactical Income Portfolio composite was created August 1, 2014. The Donoghue Forlines Global Tactical Growth Portfolio composite was created April 1, 2016. The Donoghue Forlines Global Tactical Conservative Portfolio composite was created January 1, 2018. The Donoghue Forlines Global Tactical Equity Portfolio composite was created January 1, 2018. The Donoghue Forlines Dividend Portfolio Composite was created on January 1, 2013. The Donoghue Forlines Treasury Portfolio was created on August 1, 2017. The Donoghue Forlines Momentum Portfolio Composite was created March 1, 2016. The Donoghue Forlines Dividend & Yield Portfolio Composite was created December 1, 2011. The Donoghue Forlines Growth & Income Portfolio Composite was created January 1, 2015. The Donoghue Forlines Income Portfolio Composite was created June 1, 2008.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Individual portfolio returns are calculated monthly in U.S. dollars. These returns represent investors domiciled primarily in the United States. Past performance is not indicative of future results. Performance reflects the re-investment of dividends and other earnings.

Net 3% Returns

For all portfolios, net 3% returns are presented net of a hypothetical maximum fee of three percent (3%). Actual fees applicable to an individual investor’s account will wary and no individual investor may incur a fee as high as 3%. Please consult your financial advisor for fees applicable to your account. Individual returns will vary.

Fee Schedule

The investment management fee schedule for all portfolios is: Client Assets = All Assets; Annual Fee % = 0.00%. Actual investment advisory fees incurred may vary and should be confirmed with your financial advisor.

Each portfolio includes holdings on which Donoghue Forlines may receive management fees as the advisor and/or subadvisor or from separate revenue sharing agreements. Please see the prospectuses for additional disclosures.

The investment management fee schedule for the composites is: Client Assets = All Assets; Annual Fee % = 0.00%. Actual investment advisory fees incurred may vary and should be confirmed with your financial advisor.

The Donoghue Forlines Global Tactical Allocation Benchmark is the HFRU Hedge Fund Composite. The Blended Benchmark Conservative is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% Bloomberg Global Aggregate, rebalanced monthly. The Blended Benchmark Growth is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% MSCI ACWI, rebalanced monthly. The Blended Benchmark Income is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% Bloomberg Global Aggregate, rebalanced monthly. The Blended Benchmark Equity is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% MSCI ACWI.

The MSCI ACWI Index is a free float adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The HFRU Hedge Fund Composite USD Index is designed to be representative of the overall composition of the UCITS-Compliant hedge fund universe. It is comprised of all eligible hedge fund strategies; including, but not limited to equity hedge, event driven, macro, and relative value arbitrage. The underlying constituents are equally weighted. The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. The DJ Moderately Conservative index measures the performance of returns on its total portfolios with a target risk level of Moderately Conservative-investor will take 40% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The DJ Conservative index measures the performance of returns on its total portfolios with a target risk level of Conservative-investor will take 20% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The DJ Moderate index measures the performance of returns on its total portfolios with a target risk level of Moderate investor will to take 60% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The Russell 1000 Value Index is for comparison purposes only. The index is a market-capitalization weighted index of those firms in the Russell 1000 with lower price-to- book ratios and lower forecasted growth values. The Russell 1000 includes the largest 1000 firms in the Russell 3000, which represents approximately 98% of the investable U.S. equity market. The Russell 1000 Index is for comparison purposes only. The index consists of the 1000 largest companies within the Russell 3000 index. Also known as the Market-Oriented Index, because it represents the group of stocks from which most active money managers choose. The returns for the index are total returns, which include reinvestment of dividends. Frank Russell Company reports its indices as one-month total returns. The Bloomberg US Long Treasury Index, Bloomberg US Intermediate Treasury Index, are for comparison purposes only. Bloomberg US Long Term Treasury Index measures the performance of US treasury bonds with long term maturity. The credit level for this index is investment grade. Bloomberg US Intermediate Term Treasury Index measures the performance of US treasury notes with intermediate term maturity. The credit level for this index is investment grade.

Index performance results are unmanaged, do not reflect the deduction of transaction and custodial charges or a management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. You cannot invest directly in an Index. Economic factors, market conditions and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. For a compliant presentation and/or the firm’s list of composite descriptions, please contact 800‐642‐4276 or info@donoghueforlines.com.

Donoghue Forlines LLC is a registered investment adviser with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training.