In our last commentary, we highlighted the changing macroeconomic environment and the risks to the current bull market. As a result, we de-risked our portfolios at the beginning of April. As of this writing, risk assets are roughly at the same levels. While markets bounced back in May, the short-term action does not change our view on the asymmetric risk we believe markets will face in the second half of the year. We believe there are several factors within our decision-making process that highlight these risks.

First, let’s review our golden rule of investing: “stay bullish on risk assets unless you have good reason to think that a recession is imminent”. While this oversimplifies our asset allocation process, it is the north star of all macroeconomic analysis, as equity markets and recessions go hand in hand. The catch is, of course, that it is difficult to know whether a downturn is lurking around the corner. We believe there are several “good reasons” to expect a mild recession in the back half of 2024 or early 2025.

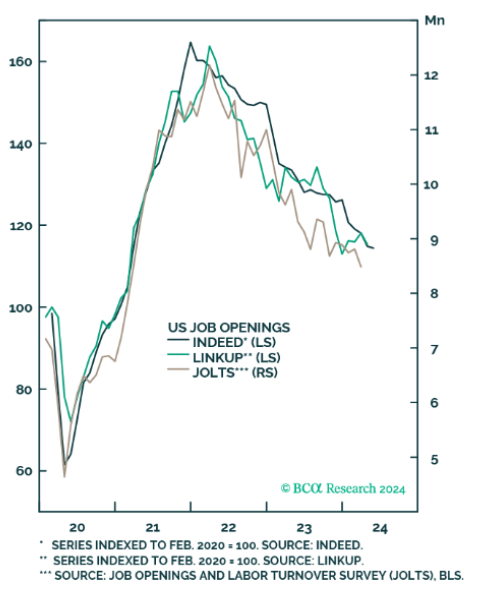

The first is that the US labor market is set to weaken abruptly. While Covid and its aftermath have distorted unemployment data, the number of job openings in the US has declined from a peak of 12.2 million in March 2022 to 8.5 million in March 2024. Alternative private-sector sources on job openings such as Indeed and LinkUp tell a similar story. (Chart 1)

Job Openings Keep Trending Lower

Chart 1 – Source: BofA Research

If job openings continue to trend lower, they will fall below where they were in 2019 by the end of 2024 or early 2025. At that point, the unemployment rate – which has already risen 0.5 percentage points from its lows – could start rising quickly.

Just as water can abruptly turn into ice if the temperature falls far enough, the economy can also freeze over if job openings fall far enough.

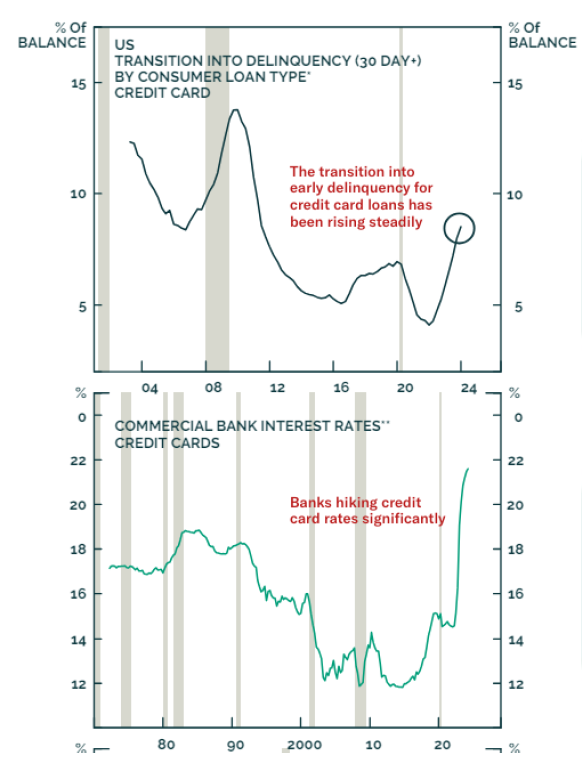

This catalyst could cause ripple effects that push the savings rate higher and lower consumption in the economy. And consumer balance sheets are already wearing thin: Consumer credit growth has come off the boil; Credit card delinquencies are already back to where they were in 2012 (when the unemployment rate was 8%). This has prompted banks to tighten lending standards and raise credit card rates to the highest rates in history. A rise in unemployment would exacerbate these issues and breed financial instability. (Chart 2)

Growing Headwinds For Consumer Borrowing

Chart 2 – Source: BCA Research

Investor’s confidence in a “soft landing” has powered gains across risk assets. It is fully priced into asset markets as the AI boom, crypto, and other speculative assets continue higher. However, this is very on brand for stocks to melt up into a hard landing. Just as investors start piling into stocks because of the “fear of missing out” on returns. While we believe a recession has likely been delayed, we do not think a harder landing is properly priced into asset markets. The economy is still digesting the effects of lagging monetary policy.

While there is scope for economic data and corporate earnings to remain resilient over the near-term and continue to support equities over a tactical investment horizon, we doubt that this resilience can be sustained over the longer term. Moreover, stock prices and valuations suggest that equities are not priced for recession, making them more vulnerable to the downside in the event of an economic downturn. Even a valuation reset back to the average of the last decade would trigger a 20% decline in indices.

Financial stability breeds instability. Stability encourages more leverage, which plants the seeds of potential squeezes and brutal collapses. We believe there are elevated odds of a mild global recession in the next 12 months, and it will eventually weigh on the price of risk assets.

This month, we did not make any changes. We maintain our underweight positioning to risk assets. We will continue to adapt as the facts change, which includes more defensive positioning if our belief in recession strengthens. We believe tactical asset allocation is now more important than ever.

Recent Portfolio Changes

You can get more information by calling (800) 642-4276 or by emailing AdvisorRelations@donoghueforlines.com.

Best regards,

Best regards, John A. Forlines III

Chief Investment Officer

Past performance is no guarantee of future results. Performance prior to January 1, 2018 was earned on accounts managed at a predecessor firm, JAForlines Global. The person primarily responsible for achieving that performance continues to manage accounts at Donoghue Forlines in a substantially similar manner. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. The investment descriptions and other information contained in this Markets in Motion are based on data calculated by Donoghue Forlines LLC and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate. The calculation and presentation of performance has not been approved or reviewed by the SEC or its staff.

The Donoghue Forlines Global Tactical Allocation Portfolio composite was created July 1, 2009. The Donoghue Forlines Global Tactical Income Portfolio composite was created August 1, 2014. The Donoghue Forlines Global Tactical Growth Portfolio composite was created April 1, 2016. The Donoghue Forlines Global Tactical Conservative Portfolio composite was created January 1, 2018. The Donoghue Forlines Global Tactical Equity Portfolio composite was created January 1, 2018.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Individual portfolio returns are calculated monthly in U.S. dollars. These returns represent investors domiciled primarily in the United States. Past performance is not indicative of future results. Performance reflects the re-investment of dividends and other earnings.

Net 3% Returns

For all portfolios, net 3% returns are presented net of a hypothetical maximum fee of three percent (3%). Actual fees applicable to an individual investor’s account will wary and no individual investor may incur a fee as high as 3%. Please consult your financial advisor for fees applicable to your account.

Fee Schedule

The investment management fee schedule for all portfolios is: Client Assets = All Assets; Annual Fee % = 0.00%. Actual investment advisory fees incurred may vary and should be confirmed with your financial advisor.

Each portfolio includes holdings on which Donoghue Forlines may receive management fees as the advisor and/or subadvisor or from separate revenue sharing agreements. Please see the prospectuses for additional disclosures.

The investment management fee schedule for the composites is: Client Assets = All Assets; Annual Fee % = 0.00%. Actual investment advisory fees incurred may vary and should be confirmed with your financial advisor.

The Donoghue Forlines Global Tactical Allocation Benchmark is the HFRU Hedge Fund Composite. The Blended Benchmark Conservative is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% Bloomberg Global Aggregate, rebalanced monthly. The Blended Benchmark Growth is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% MSCI ACWI, rebalanced monthly. The Blended Benchmark Income is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% Bloomberg Global Aggregate, rebalanced monthly. The Blended Benchmark Equity is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% MSCI ACWI.

The MSCI ACWI Index is a free float adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The HFRU Hedge Fund Composite USD Index is designed to be representative of the overall composition of the UCITS-Compliant hedge fund universe. It is comprised of all eligible hedge fund strategies; including, but not limited to equity hedge, event driven, macro, and relative value arbitrage. The underlying constituents are equally weighted. The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. The DJ Moderately Conservative index measures the performance of returns on its total portfolios with a target risk level of Moderately Conservative-investor will take 40% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The DJ Conservative index measures the performance of returns on its total portfolios with a target risk level of Conservative-investor will take 20% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The DJ Moderate index measures the performance of returns on its total portfolios with a target risk level of Moderate investor will to take 60% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices.

Index performance results are unmanaged, do not reflect the deduction of transaction and custodial charges or a management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. You cannot invest directly in an Index. Economic factors, market conditions and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. For a compliant presentation and/or the firm’s list of composite descriptions, please contact 800-642-4276 or info@donoghueforlines.com.

Donoghue Forlines LLC is a registered investment adviser with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training.