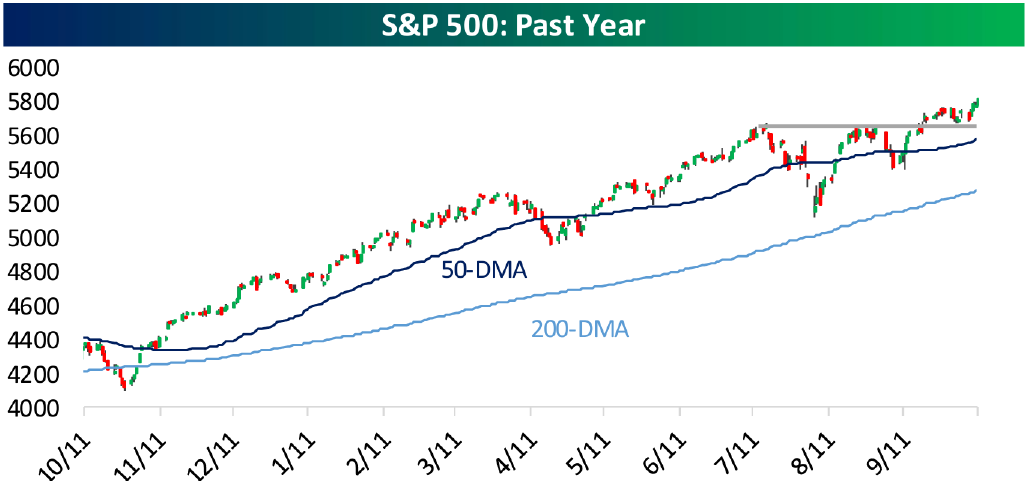

The bull market in risk assets continues to roar as we enter the late stages of 2024 (Chart 1). Asset prices seem convinced that the Federal Reserve’s easing campaign has all but assured a soft landing for the economy.

(Chart 1) Source: Bespoke

Markets are extremely momentum driven in the short-term, but over the long term are driven by fundamentals. We believe we are at a critical juncture where the short-term price action is not aligned with the long-term macroeconomics. In our view, this misalignment provides opportunity. Tactical management is essential to navigating these time periods.

We believe there is a high probability the consensus soft landing narrative is wrong, and when a catalyst emerges, could severely weigh on elevated stock prices and other risk assets. Valuations are at extreme levels and it would not take much disappointment from this starting point to provoke a drawdown.

Over the past couple months, we began to de-risk our fundamental and blended portfolios. Market momentum has kept the majority of our rules-based portfolios risk-on and is a testament to how the approaches can complement each other.

Starting Points Matter

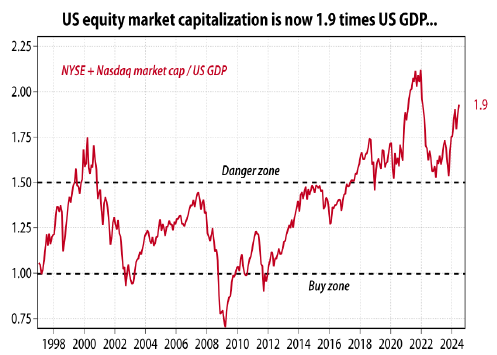

By any measure, US equity markets are expensive today. By the Warren Buffett indicator, the ratio of market capitalization to GDP, US equities are now in the top 5% of their historical range (Chart 2) (which may explain why Berkshire Hathaway is sitting on record amounts of cash). On a simpler price-to sales-ratio, US equities are also breathing rarefied air (Chart 3).

(Chart 2) Source: Gavekal Research/Macrobond

(Chart 3) Source: Gavekal Research/Macrobond

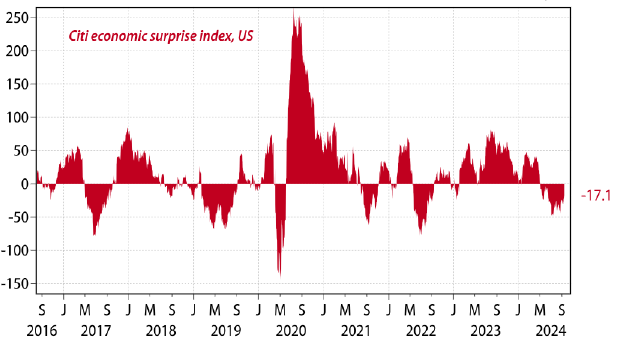

Meanwhile, for the last few months most US economic data points have come in on the soft side of expectations—and the expectations weren’t that firm to begin with (Chart 4).

In short, given stretched valuations, middling growth (with potential downside risk), and electoral uncertainty thrown in on top, we believe it is practical to begin shifting money out of equities and towards bonds over the coming weeks and months.

(Chart 4) Source: Gavekal Research/Macrobond

Ultimately it could be the markets Wile E. Coyote moment. Like the coyote, the US economy has run off the cliff; but rather than noticing the canyon below, investors are preoccupied by the shiny light of Fed easing.

Cracks in the Economy

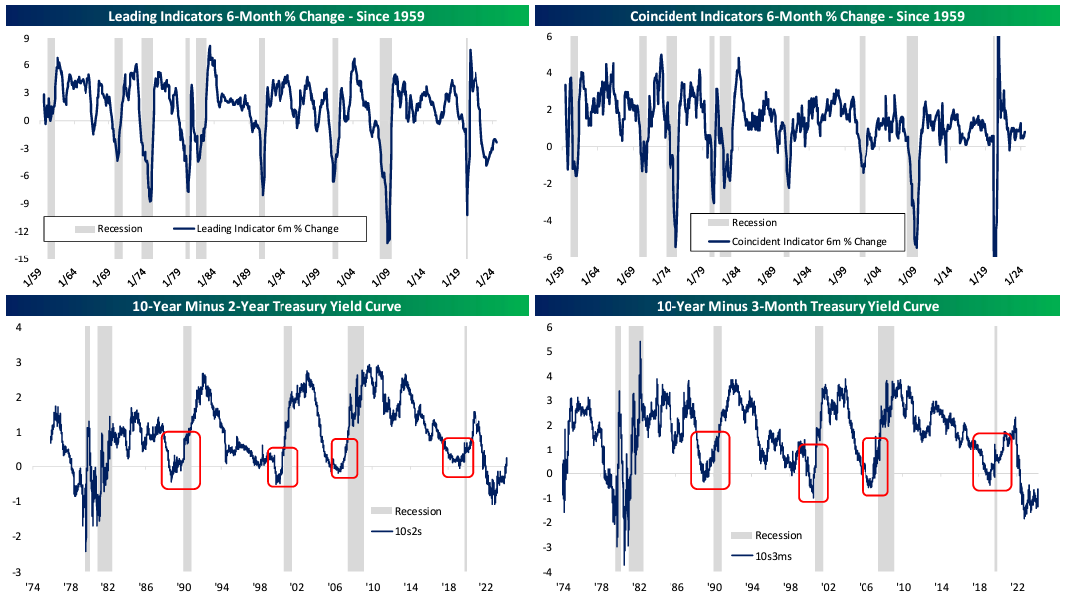

Leading indicators are down significantly in the past six months; a rate of change only observed previously in the context of recessions (Chart 5).

(Chart 5) Source: Bespoke

We believe cracks have already formed in the labor market and among the health of the consumer that are in danger of becoming recessionary. If US equities pull back, with the pull back weighing on US economic activity in what could rapidly become a self-reinforcing feedback loop.

Hold the Champagne

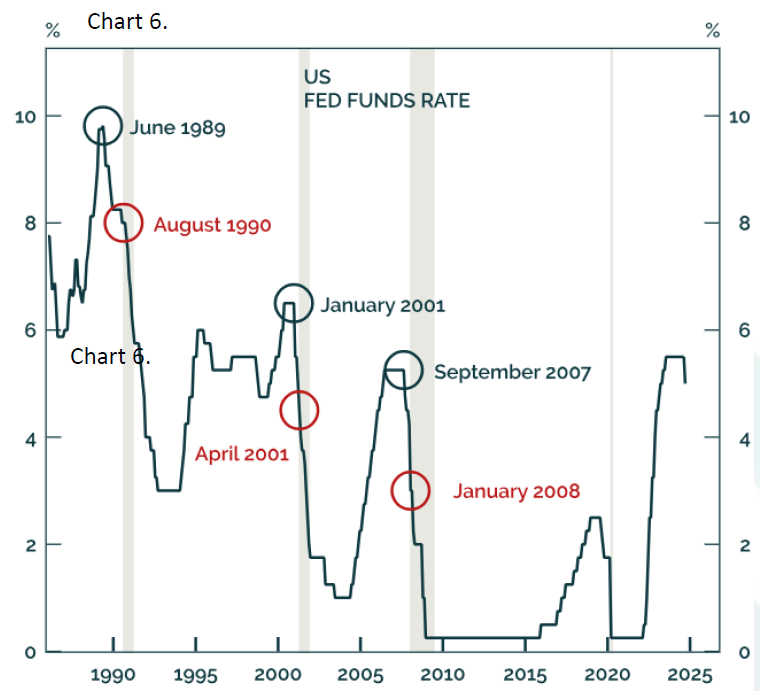

Stocks cheered after the Fed’s decision to cut rates by 50 basis points in September. The market’s reaction was similar to January 2001 and September 2007, which also marked the start of the two biggest easing cycles this century (Chart 6). In both cases, the Fed surprised investors by cutting rates by 50 basis points. In 2001, the S&P 500 gained 5.0% on the day of the unexpected rate cut. In 2007, it gained 2.9%. However, in both cases, stocks fell significantly over the subsequent months as recessions followed.

(Chart 6) Source: Federal Reserve. Note: Shaded areas denote nber-designated recessions.

In short, although never obvious, the Fed is usually behind the curve and we do not expect this time to be any different. When the Fed starts cutting rates, it is usually time to sell, not buy.

Election 2024

Meanwhile, we have a polarizing US presidential election within a month that is sure to elevate market volatility. If you are a long-time reader of ours, you know we typically like to downplay politics as an important part of our process. However, we will provide an oversimplification as to how the election pertains to the market: a Republican sweep would mean corporate tax cuts; a Democratic sweep would mean higher tax rates. Overall, on the margin, a Republican administration could be positive for equities while a Democratic administration would likely be neutral.

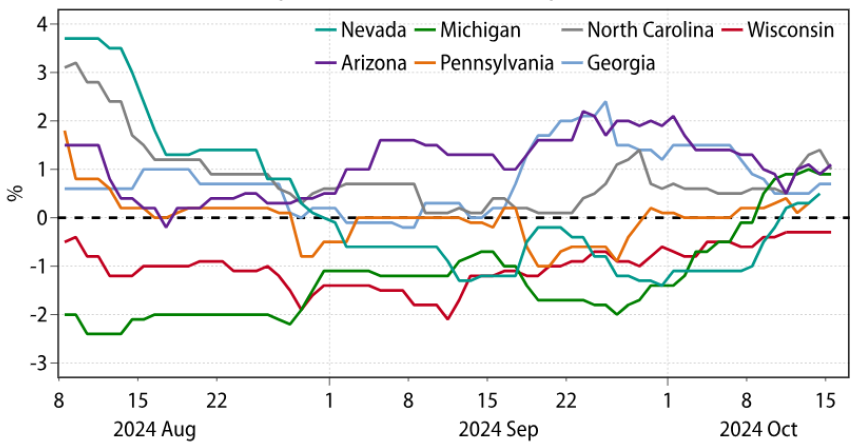

In recent days, opinion polls in the key battleground states for November’s US presidential election have firmed in favor of Donald Trump. As of October 15th, polls in six of the seven most important swing states—Pennsylvania, North Carolina, Georgia, Arizona, Nevada, Michigan—gave Trump the edge, with Wisconsin the only outlier (Chart 7).

While Trump has gained momentum, most indicators still predict the race to be extremely tight. A Republican sweep is far from a given and could provide volatility into the end of the year given market expectations.

Trump is now leading in six of the seven key battleground states

(Chart 7) Source: Gavekai Research / Macrobond

Conclusions

In markets, financial stability breeds instability. Stability encourages more leverage, which plants the seeds of potential squeezes and brutal collapses. We believe there are elevated odds of a mild global recession in the next 12 months, and that will weigh on the price of risk assets. While price action has ignored the deteriorating economic numbers, bear markets can turn quickly.

We believe starting points matter. Valuations of mega cap stocks and AI darlings have continued to build up even as cracks in the surface began to form. They are trading at extremely elevated valuations only seen in the 2000 technology bubble. Even a valuation reset back to the average of the last decade could move markets much lower.

We believe bonds will outperform stocks over the next 12 months. We believe bonds will hedge equity drawdowns and now provide yield.

We believe that tactical asset allocation will be critical to clients meeting their long-term objectives. Therefore, we continue to stress the importance of tactical management. In today’s environment, advisors are challenged to rethink foundational elements of investor portfolios – which means seeking out strategies that bolster the “core” going forward. We will continue to provide solutions for the next generation of investing.

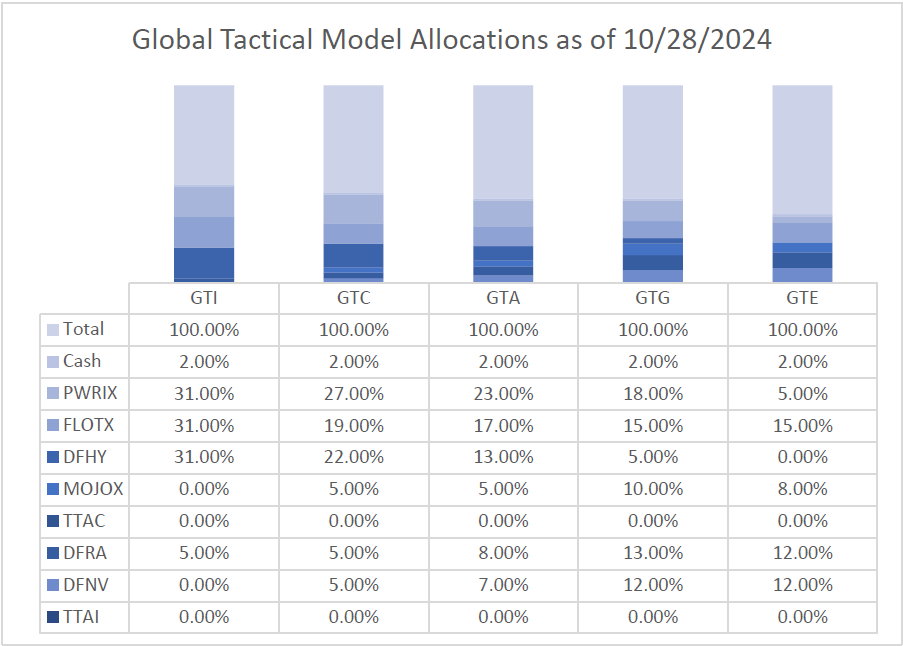

Fundamental Portfolios

As we enter the end of 2024, our portfolios are positioned underweight to risk. We removed overweight positions in equity (specifically riskier areas) and are prepared to move positioning even more defensively as the year evolves. This will include larger allocations to tactical fixed income investments across the term premium.

Recently, at the beginning of the 3rd quarter, we continued to transfer equity exposure into value-oriented areas of the market, specifically dividend stocks. We expect to increase duration across our overweight fixed income positions.

We will adapt as the facts change and focus on catalysts for investment regime change.

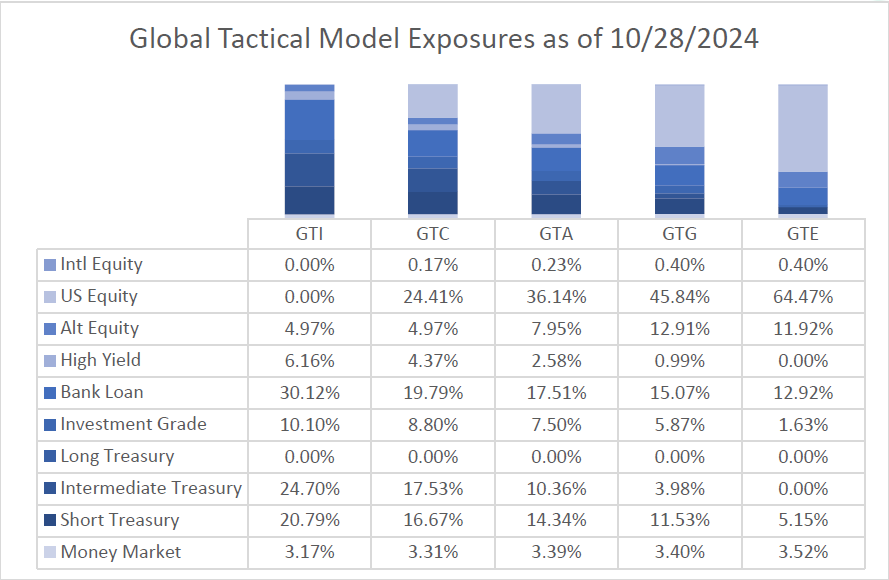

(Positioning as of 10/28/2024)

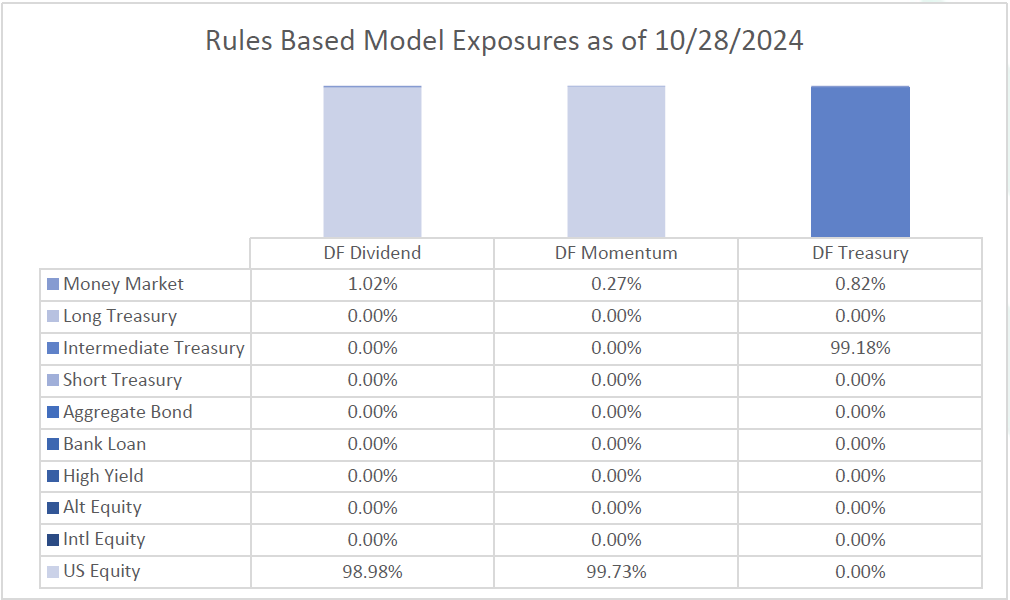

Rules Based Portfolios

The technical picture for equities remains positive with long-term trends remaining intact.

Our Momentum strategy remained fully invested in equities throughout the quarter and was able to take advantage of the risk-on environment. The strategy’s performance ranked in the top 3% in its category YTD, and in the top 5% of its category for 1-year trailing performance. The technical picture for growth stocks remains in an uptrend and would likely need to see quick price deterioration to trigger a more defensive posture.

Our Dividend strategy remained fully invested in equities throughout the quarter and was able to take advantage of the risk-on environment. The technical picture for value remains in an uptrend and would likely need to see quick price deterioration to trigger a more defensive posture. We believe dividend stocks are poised to outperform broader equities for the remainder of 2024.

Our Treasury strategy remained in shorter duration instruments for the entirety of the quarter. Rate volatility is still significant and we have avoided long duration bonds. We expect to allocate to longer duration bonds more frequently for the remainder of 2024.

(Positioning as of 10/28/2024)

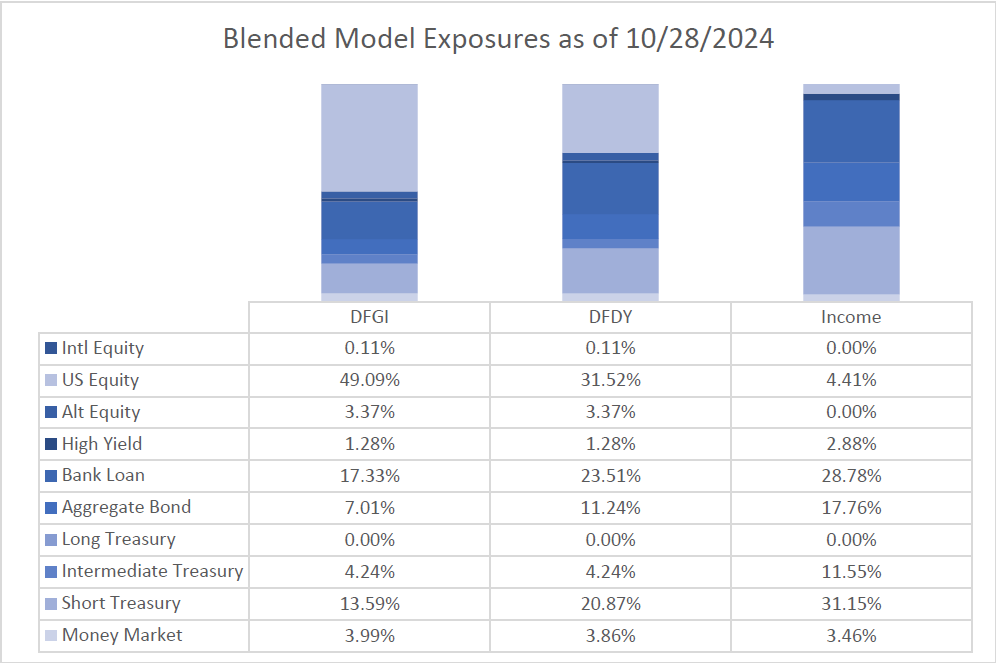

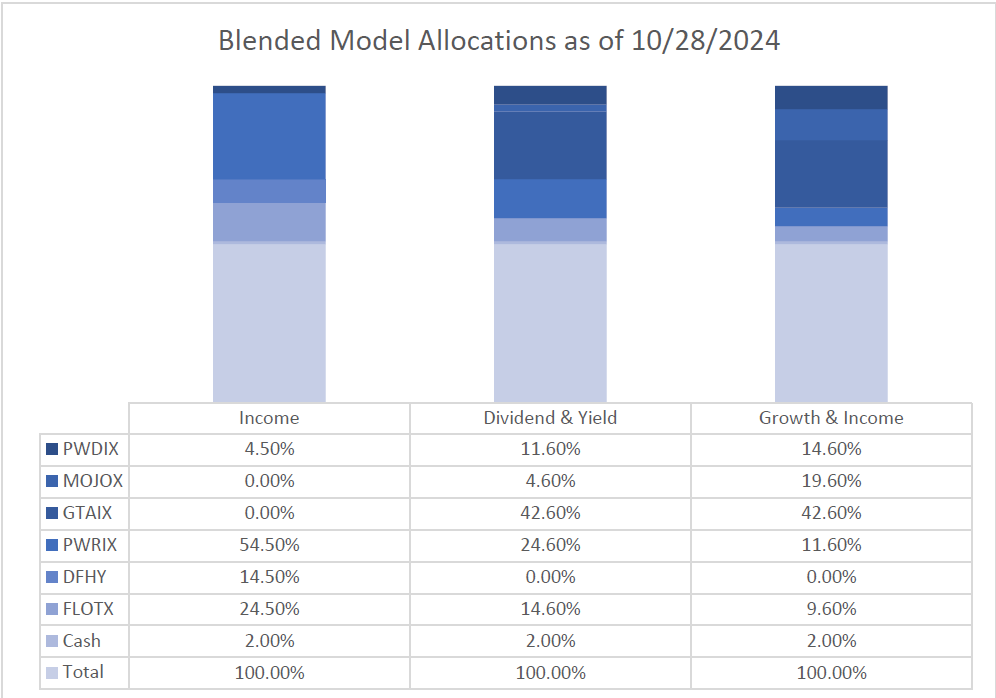

Blended Portfolios

The blended portfolios are a proprietary mix of our fundamental macro portfolios and our rules-based quantitative portfolios.

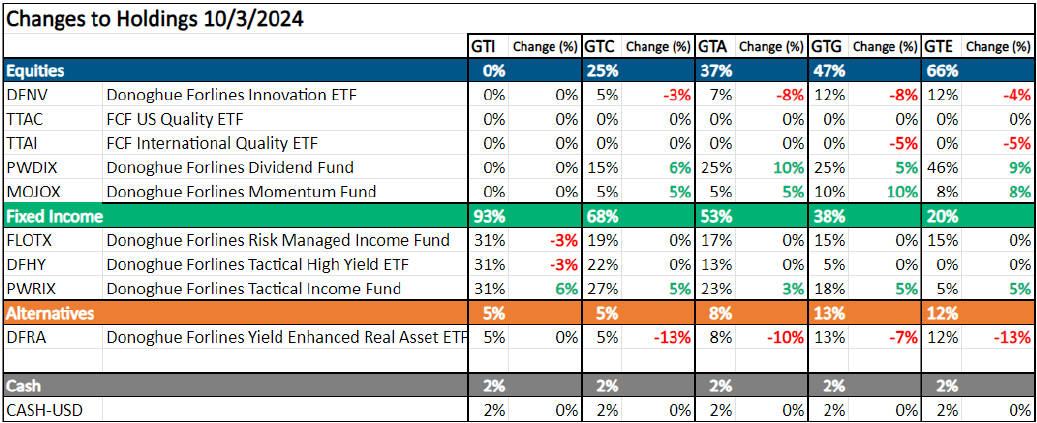

Through this combination, we were able to take advantage of the sanguine risk environment in the third quarter of 2024. Our top-down asset allocation mirrored our fundamental outlook as we overweighted our tactical allocation and tactical income funds in the strategies, where we are now underweight risk in equities & credit. Our momentum fund was a powerful driver of performance.

Heading into the rest of 2024 our top-down asset allocation mirrors our fundamental outlook – positioned underweight to risk. Our equity rules-based strategies are currently fully invested, and our risk managed income fund is positioned in high yield bonds and floating rate securities. We recently decreased allocations to our equity funds, selling out of our momentum fund, and increased allocations to tactical fixed income funds.

We will adapt as the facts change and focus on catalysts for investment regime change.

(Positioning as of 10/28/2024)

You can get more information by calling (800) 642-4276 or by emailing AdvisorRelations@donoghueforlines.com.

Best regards,

Best regards,

John A. Forlines III

Chief Investment Officer

IMPORTANT RISK INFORMATION

Past performance is no guarantee of future results. Performance prior to January 1, 2018 was earned on accounts managed at a predecessor firm, JAForlines Global. The person primarily responsible for achieving that performance continues to manage accounts at Donoghue Forlines in a substantially similar manner. The material contained herein as well as any attachments is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies, opportunities and, on occasion, summary reviews on various portfolio performances. The investment descriptions and other information contained in this Markets in Motion are based on data calculated by Donoghue Forlines LLC and other sources including Morningstar Direct. This summary does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be relied upon in connection with any offer or sale of securities. The views expressed are current as of the date of publication and are subject to change without notice. There can be no assurance that markets, sectors or regions will perform as expected. These views are not intended as investment, legal or tax advice. Investment advice should be customized to individual investors objectives and circumstances. Legal and tax advice should be sought from qualified attorneys and tax advisers as appropriate. The calculation and presentation of performance has not been approved or reviewed by the SEC or its staff.

The Donoghue Forlines Global Tactical Allocation Portfolio composite was created July 1, 2009. The Donoghue Forlines Global Tactical Income Portfolio composite was created August 1, 2014. The Donoghue Forlines Global Tactical Growth Portfolio composite was created April 1, 2016. The Donoghue Forlines Global Tactical Conservative Portfolio composite was created January 1, 2018. The Donoghue Forlines Global Tactical Equity Portfolio composite was created January 1, 2018. The Donoghue Forlines Dividend Portfolio Composite was created on January 1, 2013. The Donoghue Forlines Treasury Portfolio was created on August 1, 2017. The Donoghue Forlines Momentum Portfolio Composite was created March 1, 2016. The Donoghue Forlines Dividend & Yield Portfolio Composite was created December 1, 2011. The Donoghue Forlines Growth & Income Portfolio Composite was created January 1, 2015. The Donoghue Forlines Income Portfolio Composite was created June 1, 2008.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Individual portfolio returns are calculated monthly in U.S. dollars. These returns represent investors domiciled primarily in the United States. Past performance is not indicative of future results. Performance reflects the re-investment of dividends and other earnings.

Net 3% Returns

For all portfolios, net 3% returns are presented net of a hypothetical maximum fee of three percent (3%). Actual fees applicable to an individual investor’s account will wary and no individual investor may incur a fee as high as 3%. Please consult your financial advisor for fees applicable to your account. Individual returns will vary.

Fee Schedule

The investment management fee schedule for all portfolios is: Client Assets = All Assets; Annual Fee % = 0.00%. Actual investment advisory fees incurred may vary and should be confirmed with your financial advisor.

Each portfolio includes holdings on which Donoghue Forlines may receive management fees as the advisor and/or subadvisor or from separate revenue sharing agreements. Please see the prospectuses for additional disclosures.

The investment management fee schedule for the composites is: Client Assets = All Assets; Annual Fee % = 0.00%. Actual investment advisory fees incurred may vary and should be confirmed with your financial advisor.

The Donoghue Forlines Global Tactical Allocation Benchmark is the HFRU Hedge Fund Composite. The Blended Benchmark Conservative is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% Bloomberg Global Aggregate, rebalanced monthly. The Blended Benchmark Growth is a benchmark comprised of 80% HFRU Hedge Fund Composite and 20% MSCI ACWI, rebalanced monthly. The Blended Benchmark Income is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% Bloomberg Global Aggregate, rebalanced monthly. The Blended Benchmark Equity is a benchmark comprised of 60% HFRU Hedge Fund Composite and 40% MSCI ACWI.

The MSCI ACWI Index is a free float adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The HFRU Hedge Fund Composite USD Index is designed to be representative of the overall composition of the UCITS-Compliant hedge fund universe. It is comprised of all eligible hedge fund strategies; including, but not limited to equity hedge, event driven, macro, and relative value arbitrage. The underlying constituents are equally weighted. The Bloomberg Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. The DJ Moderately Conservative index measures the performance of returns on its total portfolios with a target risk level of Moderately Conservative-investor will take 40% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The DJ Conservative index measures the performance of returns on its total portfolios with a target risk level of Conservative-investor will take 20% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The DJ Moderate index measures the performance of returns on its total portfolios with a target risk level of Moderate investor will to take 60% of all stock portfolio risk. Its portfolios include three major asset classes: stocks, bonds and cash. The weightings are rebalanced monthly to maintain the target level. The index is subset of the global series of Dow Jones Relative Risk Indices. The Russell 1000 Value Index is for comparison purposes only. The index is a market-capitalization weighted index of those firms in the Russell 1000 with lower price-to- book ratios and lower forecasted growth values. The Russell 1000 includes the largest 1000 firms in the Russell 3000, which represents approximately 98% of the investable U.S. equity market. The Russell 1000 Index is for comparison purposes only. The index consists of the 1000 largest companies within the Russell 3000 index. Also known as the Market-Oriented Index, because it represents the group of stocks from which most active money managers choose. The returns for the index are total returns, which include reinvestment of dividends. Frank Russell Company reports its indices as one-month total returns. The Bloomberg US Long Treasury Index, Bloomberg US Intermediate Treasury Index, are for comparison purposes only. Bloomberg US Long Term Treasury Index measures the performance of US treasury bonds with long term maturity. The credit level for this index is investment grade. Bloomberg US Intermediate Term Treasury Index measures the performance of US treasury notes with intermediate term maturity. The credit level for this index is investment grade.

Index performance results are unmanaged, do not reflect the deduction of transaction and custodial charges or a management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. You cannot invest directly in an Index. Economic factors, market conditions and investment strategies will affect the performance of any portfolio, and there are no assurances that it will match or outperform any particular benchmark.

Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. For a compliant presentation and/or the firm’s list of composite descriptions, please contact 800‐642‐4276 or info@donoghueforlines.com.

Donoghue Forlines LLC is a registered investment adviser with the United States Securities and Exchange Commission in accordance with the Investment Advisers Act of 1940. Registration does not imply a certain level of skill or training.